What You Can Do To Qualify for a Homeowner Insurance Policy Discount

There are several homeowner’s insurance discounts that are applicable when you initially purchase your policy. For instance, if your house is new it might require less repairs in particular sections, such as the roof in comparison to an older house. Insurers will take that into account when they set your insurance, so you might already be enjoying some policy discounts.

You may receive other insurance discounts after upgrading your house or attaining particular milestones, for example after you have finish paying your mortgage. It is crucial to know your insurers limit when it comes to protection discounts. Insurance companies differ in the way they compute their homeowner’s insurance policy premiums and discounts, and some companies place a cap on the final discount that a policyholder might get. AIG, for instance, has placed a 15% ‘protection credit’ limit on the total homeowner policy premium. This means you will not get additional discounts when you reach that limit.

Below are common methods you can use to qualify for a homeowner’s insurance policy discount, either after installing an upgrade or at the commencement of your insurance policy.

Bundling your auto and home insurance policies

Most insurance companies provide a discount to those policyholders that bundle their auto and home insurance policies. If, for instance, you took out a State Farm auto insurance policy and then you added a home insurance policy, the company will give you an annual discount of a maximum of $825 on the premium that you will pay on your home insurance policy.

Whereas a good number of people bundle their auto and home insurance policies it is also possible to bundle other insurance policies. AIG, for instance, will give you a discount if you bundle your floater policy with your private property policy, like an art item with your home insurance policy. Any homeowner who bundles their AIG policies qualify for a discount not to exceed 12 percent.

Request for a loyalty discount

Companies that offer home insurance often reward their long-standing clients with loyalty discounts. If you are a good customer and you stay claim-free, most insurance companies will lower the cost of your premiums every year. Remaining claim-free will keep on increasing your discount up to a certain limit. For instance, State Farm provides a 24 percent discount to clients that stick with the company for 9 years as long as they do not make any claims in the five years before they became policyholders.

In case you find that your homeowners insurance premiums have increased with time, this does not simply that you’re not getting the discount. The rates of your policy might increase as time passes by because of the increasing age of your house and the increasing probability of lodging a claim. But your loyalty discount might still be reflected in the rates you are being charged. If you are unsure about whether you are receiving a discount, ask your insurance agent to clarify.

Request for a roof discount

Hailstones and other falling objects may cause considerable damage to your room and this can be expensive for your insurer to repair. Due to this, insurance companies frequently provide discounts to policyholders whose homes are constructed using hail-resistant roofs.

Hailstones and other falling objects may cause considerable damage to your room and this can be expensive for your insurer to repair. Due to this, insurance companies frequently provide discounts to policyholders whose homes are constructed using hail-resistant roofs.

Not all impact-resistant beauty building materials get the same number of discounts. Materials are required to be tested and given a rating that ranges from class one 2 class 4. Class 4 materials get the biggest discount. If your house is constructed using impact-resistant roof shingles or if the roof is made using metal, ask your insurance agent if you are eligible for a discount. Today, homeowners in 27 states are eligible for discounts because they have used impact resistant roofs.

Enhancing your credit score

In most states, insurers are permitted to take your credit score into account when setting the rates for your policy. Your credit rating will depend on the type of debts, the amount of debts and whether you make your payments promptly, among other factors. Having a revolving debt on your credit card and using high levels of credits has a negative effect on your credit score. It is hard to improve your credit score overnight. But if you clear your revolving debt and pay other loans promptly, you can enhance your credit score, and this will enable you to get better rates on your home insurance policy.

Smart smoke alarms Installation

Many people do not remember to check their smoke alarms regularly. This is the reason why topnotch smoke alarm systems like Nest Protect link up with your insurer using Wi-Fi to notify them that the system is functioning properly.

Many people do not remember to check their smoke alarms regularly. This is the reason why topnotch smoke alarm systems like Nest Protect link up with your insurer using Wi-Fi to notify them that the system is functioning properly.

For this reason, insurers can give you a discount of up to 5 percent on your annual premium payments when you install a smart smoke system. Supposing you have a smart smoke alarm system and you purchase a $1000 annual policy. The system can pay for itself in just three years while at the same time improve your home’s security. In addition, you can get a discount if you include fire extinguishers in the home.

Get 10 FREE QUOTES from Top-Rated Insurance Companies

Inform your Insurer if you install a fire sprinkler system

Installation of a fire sprinkler system could cost more than the amount of discount you may get on your home insurance for the first 60 years after you install it. The National Fire Protection Association says that installing a fire sprinkler system costs about $1.35 for each square foot that is covered or $6026 for every system that is installed. If you are installing a sprinkler system to upgrade an already-built house, you may incur higher costs. A sprinkler system can help to avert loss of life and property. You might also have bought a home with a pre-installed system. People who are not familiar with residential fire sprinkler systems are often worried that the sprinkler system can switch on and flood the house and damage all the personal items inside. This is not true. A sprinkler system will activate on its own when temperatures ranging from 135 to 165 degrees Fahrenheit are detected. If you have installed a fire sprinkler system in your house, notify your insurance agent about it and request for a discount. You can get savings of up to 10 percent on your annual homeowner’s insurance policy premiums.

Installation of a fire sprinkler system could cost more than the amount of discount you may get on your home insurance for the first 60 years after you install it. The National Fire Protection Association says that installing a fire sprinkler system costs about $1.35 for each square foot that is covered or $6026 for every system that is installed. If you are installing a sprinkler system to upgrade an already-built house, you may incur higher costs. A sprinkler system can help to avert loss of life and property. You might also have bought a home with a pre-installed system. People who are not familiar with residential fire sprinkler systems are often worried that the sprinkler system can switch on and flood the house and damage all the personal items inside. This is not true. A sprinkler system will activate on its own when temperatures ranging from 135 to 165 degrees Fahrenheit are detected. If you have installed a fire sprinkler system in your house, notify your insurance agent about it and request for a discount. You can get savings of up to 10 percent on your annual homeowner’s insurance policy premiums.

Stop smoking

The weight attached to smoking-related risk differs from one homeowner insurance company to another. Your insurer might consider your home to have a higher risk of catching fire if there is smoker living there. Besides the risk posed by unattended or dropped cigarettes, kids are more likely to get more access to lighters or matches if there is a smoker in the home. The National Fire Protection Association (NFPA) reports that fire departments in the US were called in to deal with about 90,000 fires that were linked to smoking during the year 2011.These fires caused approximately 1640 injuries,540 deaths and property damages valued at $621 million. If you are a smoker, you may pay from 1 percent to 15 percent higher insurance premiums when compared to person who does not smoke.

Furthermore, kicking your smoking habit can lower your life and health insurance premiums, not to mention reduce your weekly expenditure.

Notify your insurance company when you install a central alarm system

The service fee you pay every month for a central alarm system (the type that alerts emergency or security in case of a burglary or fire) is higher than the discount that your insurer would give you. But you might still opt to install an alarm system to enhance the security in your home. You could get a discount of up to ten percent on the annual premiums that you pay for your home insurance policy.

The service fee you pay every month for a central alarm system (the type that alerts emergency or security in case of a burglary or fire) is higher than the discount that your insurer would give you. But you might still opt to install an alarm system to enhance the security in your home. You could get a discount of up to ten percent on the annual premiums that you pay for your home insurance policy.

A home that has local burglar alarm system (the type that only alerts those people in the immediate neighborhood) or deadbolt locks might not be eligible for a home insurance discount. It is always advisable to ask your insurance agent. They can sometimes use their discretion to give discounts

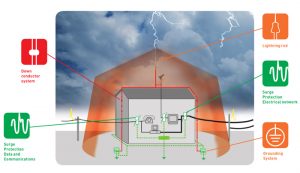

Inform your insurance company when you install a lightning protection system

A single bolt of lightning can generate electrical energy equivalent to 30 million volts. This can easily set a home on fire or damage electronic equipment in the home. The Insurance Information Institute reported that in 2016, paid lightning claims in the United States totaled $109,049 and on average each claim was worth $7571.90. Homes that are equipped with lightning protection systems receive a discount on their insurance policies.

AIG for example gives a 3% discount if your home has a lightning protection system. However, installing the system costs around $1200 even though it may cost you more than this depending on the material used and number of rods you require for the installation. Supposing your annual home insurance premium comes to $1000 and you are eligible for a 3% discount after you install a lightning protection system that costs $1200. This translates to savings of $30 every year, which means it could take 40 years for the savings to match the installment cost. But if you have bought a house with a pre-installed lightning protection system, you need to get in touch with your insurance agent and request a discount.

AIG for example gives a 3% discount if your home has a lightning protection system. However, installing the system costs around $1200 even though it may cost you more than this depending on the material used and number of rods you require for the installation. Supposing your annual home insurance premium comes to $1000 and you are eligible for a 3% discount after you install a lightning protection system that costs $1200. This translates to savings of $30 every year, which means it could take 40 years for the savings to match the installment cost. But if you have bought a house with a pre-installed lightning protection system, you need to get in touch with your insurance agent and request a discount.

Notify your Insurer if you are retired

Nearly all burglaries and other major hazards, like fires, occur when there is no one at home to detect the danger. For this reason, families where people are in the working ages pose a greater risk to the insurers than homeowners that have retired residents because retired people are at home more regularly. In case you are newly retired, contact your home insurance agent and you will probably get a discount.

Selecting the appropriate coverage and deductibles

One of the easiest methods of reducing your monthly premiums for your homeowner’s insurance policy is opting for a higher deductible. A deductible is the money you need to pay for a repair before your insurance policy begins to pay. If your house is in sound condition and it is less likely to face hazards in the following year, this may be the best strategy for you. But if you own an older home or one that is situated in an area that is susceptible to risks, choosing a higher deductible might eventually cost you more if you need to file a claim. Irrespective of the amount of your deductible, you need to consider the potential cost when you are working out how much money you require in your savings account.

Choosing coverage limits

The premiums on your homeowner’s insurance policy will be determined by any of three policy limits based on your home’s total value.

Actual Cash Value (ACV)

This refers to the market value of your home, less depreciation. For instance, if the roof that you installed at a cost of $20,000 twenty years ago was completely torn down by a hurricane, your insurance policy may not pay you the entire $20,000 for replacement. The wear and tear after twenty years has reduced the value of the roof and this means the reimbursement amount will be considerably less than the money it might cost to replace the roof currently because you would get the actual cash value of your roof today. You would then be required to pay for the difference in price. But opting for a homeowner’s insurance policy that has an ACV limit is the most affordable alternative if you wish to reduce premiums on your homeowner’s insurance policy.

Replacement Cost Value (RCV)

This is simply the money it could cost to replace your house today. Although it is costlier than an insurance policy that has an ACV limit, insuring the replacement cost value of your home can stop you from having to pay a considerable amount in case your home gets destroyed completely by a risk that is covered, for example a fire.

Get 10 FREE QUOTES from Top-Rated Insurance Companies

Guaranteed Replacement Cost (GRC) or Extended Replacement Cost (ERC)

This is the costliest limit that you can select for your homeowner’s insurance policy. But it provides an assurance that your insurer will pay a stipulated percentage over the replacement value of your home in case a regional hazard, for example a hurricane, briefly causes the cost of materials and labor in your area to go up. In case your existing policy has a GRC (ERC) limit and you wish to reduce the premiums on your home insurance, you can consider reducing the policy limit to the Replacement Cost Value of your home. But a homeowner who lives in an area that is susceptible to disasters might want to pay for the added coverage.

We suggest that homeowners get Replacement Cost Value coverage at the minimum if they are able to pay for it.

Knowing when to file a claim

Each time you file a claim with your insurer you will probably notice an increase in the policy premiums when renewing your homeowner’s insurance policy. This is particularly true when making a claim for damages that arose due to your actions, for instance if you accidentally spark off a fire when smoking a cigarette. People who file several claims over a few years will experience an even bigger increase in the premiums they pay. Due to the financial effects of filing a claim, it may be cheaper to pay for some repairs from your own pocket.

Each time you file a claim with your insurer you will probably notice an increase in the policy premiums when renewing your homeowner’s insurance policy. This is particularly true when making a claim for damages that arose due to your actions, for instance if you accidentally spark off a fire when smoking a cigarette. People who file several claims over a few years will experience an even bigger increase in the premiums they pay. Due to the financial effects of filing a claim, it may be cheaper to pay for some repairs from your own pocket.

For instance, if you make a claim on your home insurance policy for $1250 but you have a $1000 deductible, the insurer will only reimburse you $250. But when you go to renew your policy you might find that your rates are higher by 10 percent when compared to the previous year. In this scenario, your higher premiums could eventually cost you more than the amount of money you were reimbursed.

A homeowner’s insurance policy is intended to be a safety net whenever disastrous incidents occur, not to cater for your home’s routine maintenance. Think about the deductibles and higher premiums each time you are weighing whether it is practical to file a claim.