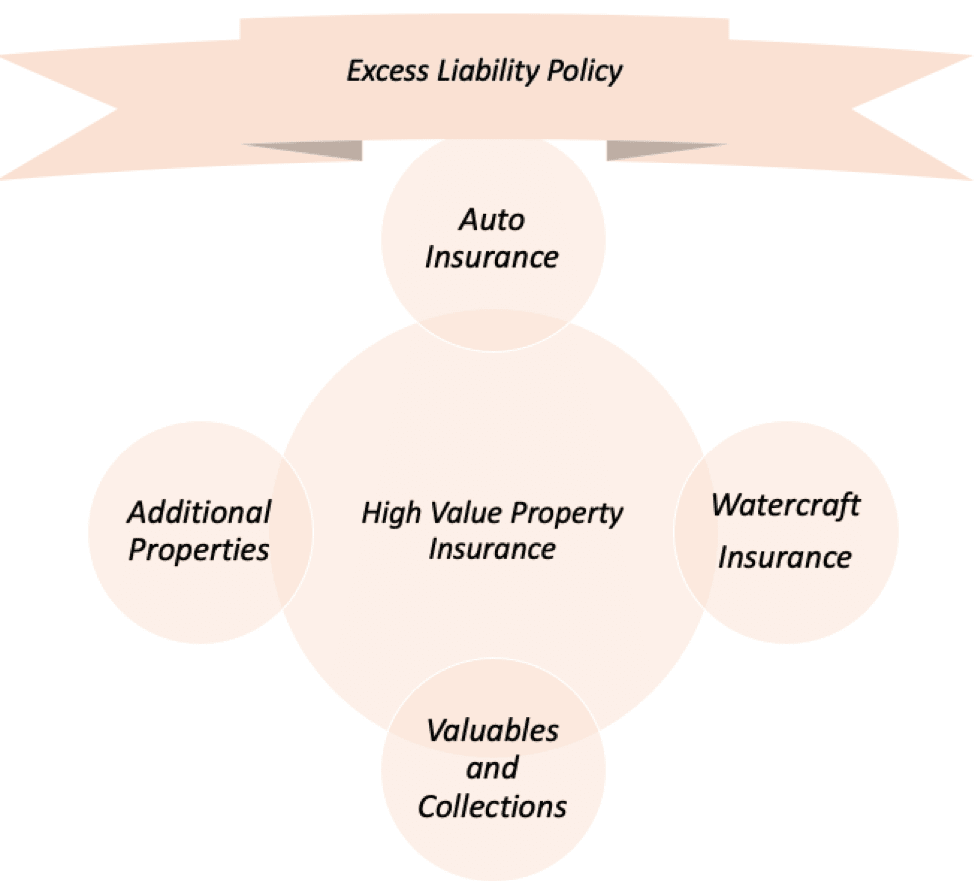

While it sounds like one policy, in practice, high-net-worth insurance is typically comprised of two or more policies that work together to provide both property insurance and liability protection. You might also see this structure referred to as a high-net-worth insurance package, suggesting more than one type of coverage.

At the core of a high-net-worth insurance package, you’ll find a high-value home insurance policy. These policies are available for fine homes with a rebuild value of $1 million or more but bring a number of enhancements when compared to a standard home insurance policy, including higher coverage limits and a flexible structure that allows more customization.

High Net Worth Insurance Key Takeaways:

High-net-worth insurance usually refers to multiple policies that work to protect a wide range of personal risks.

- High-value home insurance protects custom homes with a rebuild value of $1 million or more.

- Policyholders can add coverage for second homes or vacation homes as needed.

- A high-net-worth package can include a policy to protect luxury autos or auto collections.

- Policyholders can add coverage for yachts, boats, or watercraft as needed.

- An excess liability insurance policy can extend coverage limits for other policies in your package, allowing extended coverage limits of up to $50 million or more.

- Customized liability coverage options allow you to tailor your protection to match your unique risks.

- Individual policies within a high-net-worth insurance package may be from different insurance providers; some insurers may offer better coverage options or price advantages for a given policy type.

Liability Coverage: Protecting the Biggest Potential Exposures

In an insurance context, liability refers to our financial responsibility for harm caused to others. One common example might be accidental injuries sustained by visitors to your home. Animal bites are another common type of liability claim.

Many high-net-worth households identify liability risk as their biggest concern, and with good reason: stakes are high.

The risk of a financial loss due to property damage is effectively limited to the value of the property. While this amount can be significant, it has a cap. A $5 million home destroyed by a rogue storm can’t cause a $50 million loss. Liability risks, however, aren’t limited to a defined value like a home or a car. Potential losses can be much higher and impossible to predict.

But a well-thought-out liability insurance strategy lets your plan for the unexpected. An excess liability insurance policy protects against impossible-to-predict risks affordably. And with personalized liability coverage at its center, high-net-worth insurance becomes lifestyle insurance rather than just insurance for your home or your vehicles.

While a high-net-worth insurance package can contain several policies, possibly from multiple insurance providers, an excess liability policy brings all these policies together by extending the liability coverage limits of the underlying policies.

For example, home and auto policies typically cap the maximum liability coverage limit at a level that may not be sufficient for high-net-worth households with more at risk. In New York, some standard auto policies enforce a maximum combined single limit of $500,000. But an excess liability insurance policy offers a cost-effective way to extend auto or home liability coverage limits to offer robust protection.

The underlying policy provides coverage first. So, in a covered auto liability claim, the auto policy pays first. If the liability loss exceeds the coverage limit of the auto policy, the excess liability policy’s coverage is triggered, providing protection up to the limits you’ve chosen.

This structure allows you to stack coverage much higher with a lower cost per dollar of coverage. In effect, the underlying policy bears the risk for smaller losses, meaning the excess policy is less likely to be pressed into service. But, like a silent sentry, your excess liability policy is there when you need the protection.

Excess liability policies come in two basic forms, the most common of which is called an umbrella policy. A simple excess liability policy just extends coverage limits, whereas an umbrella policy extends coverage limits while also adding coverage for libel and slander, risks that aren’t covered by a home policy’s liability protection.

You’ll also have the option to add coverage for liability risks unique to your household, such as cyber-liability risks, liability risks associated with domestic employees, or risks associated with serving on a board.

High-Value Home Insurance

As a core component of a high-net-worth insurance package, a high-value home insurance policy provides coverage for homes with a rebuild value of $1 million or higher. But this specialized policy also offers flexible coverage for personal property, meaning the furnishings and possessions that make a luxury house a home.

Your home is your castle, and some homes feature palatial grounds, including intricate hardscaping and additional buildings. Other homes might take a minimalistic approach, instead investing in art or other valuables that need specialized coverage.

A high-value home insurance policy can address either of these coverage needs (or both), allowing you to invest your premiums where you need the most protection.

By comparison, traditional home insurance policies designed for broad market needs follow strict constraints, setting coverage limits for personal property or additional structures at a fixed percentage of the home’s insured value. High-value policies, on the other hand, let you address these and other potentially costly coverage gaps with flexible policy language that allows fine-tuned customization.

You’ll also find options to choose higher deductibles. Because deductibles are the part of the claim paid by the insured, this strategy acts as a limited form of self-insurance that helps keep premium costs down while preserving your coverage for larger losses.

A high-value home insurance policy provides basic personal liability insurance coverage, but a high-net-worth insurance package allows you to extend this base coverage to protect against additional risks and offers higher coverage limits.

Valuables and Collections

Some successful households own a lot of personal property while families have fewer belongings. But in either case, some items likely need more protection than others.

As part of your high-value home insurance policy, you’ll enjoy generous coverage limits for your belongings. But you’ll also find additional ways to protect the items most precious to you, such as art, jewelry, or collections.

A personal articles floater or equivalent endorsement lets you insure specific valuables to their full replacement cost with no deductible or deduction for depreciation. In addition, with scheduled coverage for specific valuables, you’ll benefit from coverage against a wider range of risks.

For instance, standard coverage typically excludes claims for “mysterious disappearance,” which refers to a loss in which the insured can’t explain what happened to a missing item. With scheduled coverage, a treasured ring that goes missing is protected against this type of loss as well as many others.

Again, you can invest your premiums where you need the most protection, shaping your policies to safeguard your lifestyle while also keeping insurance costs in check.

Coverage for Second Homes

Many high-net-worth households own more than one home. Your trusted high-value insurance advisor can guide you through your options to protect vacation homes or second homes, or even homes outside the US.

An umbrella or excess liability policy protects you in this situation as well, providing coverage for you and your family members that extends to second homes or when traveling anywhere in the world.

Insurance for Luxury Autos or Collections

Owners of luxury cars and exotics have more to protect, and a high-net-worth insurance package offers specialized coverage that can insure high-value autos or even auto collections.

Both auto and home policies are “package” policies, meaning they provide more than one type of coverage (property and liability). But an insurance package refers to a combination of these policies with excess liability insurance as the common thread.

Whether a high-tech supercar, a hand-built luxury sedan, or a pristine classic of yesteryear, high-net-worth insurance provides ways to protect your high-value automobiles and automotive collections.

Watercraft Insurance

From catamarans to cabin cruisers to yachts or even jet skis, each type of boat or personal watercraft can have different insurance considerations. High-net-worth insurance packages allow you to customize your coverage to protect your unique lifestyle.

Your policy can safeguard your boats while also insuring against risks such as wreckage removal and fuel spills. And, as with your other personal insurance policies, an excess liability insurance policy or umbrella policy wraps your coverage with a neat bow, bringing higher coverage limits designed to protect the success you’ve built.

High-Net-Worth Insurance to Fit Your Unique Lifestyle

Successful households have different coverage needs, but priorities often overlap in the area of liability coverage. High-net-worth insurance packages offer a way to personalize your protection to suit your individual lifestyle while providing several ways to insure against what is often the single biggest potential risk: liability.

At Coastal Insurance, we work with high-net-worth individuals and families across the nation to build a comprehensive insurance package that addresses their specific needs without compromise. As an independent insurance agency specializing in high-value coverage, we’ve partnered with the finest insurers in the country to bring you customized coverage at the best prices possible.

If you need coverage or it’s time for an insurance review, reach out to our experienced advisors to learn the best ways to safeguard your home and family. Protecting your legacy is our top priority.

High Value Home Insurance Articles

- Alternative High-Value Home Insurance

- Top High Net Worth Insurance Companies

- Do you Need Private Client Insurance?

- How Much Does it Cost to Insure a Multimillion-Dollar Home?

- 5 Best Insurance Companies for High-End, Upscale Residential Home Insurance

- Your High Value Home Insurance Rates Are Going Up – Here’s Why

About the Author

David W. Clausen is the CEO of Coastal Insurance Solutions. With over 20 years' experience and over 1 billion insured, David and Coastal Insurance Solutions are the recognized leaders in high net worth insurance. For the fifth consecutive year, David Clausen has been awarded Top Producer by Insurance Business America. David is a trusted high net worth insurance expert who’s published more than 200 articles. His articles & press releases have generated over 500K pageviews and has been featured on blogs such as Google News, Yahoo Finance, CNBC, Market Watch, Fox, The New York Times, etc. David founded Coastal Insurance Solutions in 2001 after earning a BBA from the State University of New York College at Oswego.