Valley Stream NY Homeowners Insurance: Complete Coverage Guide

Homeowners insurance provides financial protection for property owners against a range of perils. In Valley Stream, NY, exposure to flood and windstorm hazards requires careful assessment of policy scope and exclusions. This guide examines common policy forms, available coverages, and the practical considerations local homeowners should evaluate to select appropriate protection for their property and assets.

Key Takeaways

- Valley Stream homeowners insurance must address unique risks like flooding and windstorm damage for adequate protection.

- HO-3 policies offer broad coverage but exclude flood damage, requiring separate flood insurance for coastal properties.

- Essential coverage options include dwelling, personal property, liability protection, and critical flood insurance.

- Choosing appropriate coverage limits ensures sufficient protection, including replacement cost and specialized personal property coverage.

- Liability coverage protects homeowners from legal claims related to injuries or property damage on their premises.

- Mitigation strategies like higher deductibles and security systems can help reduce homeowners insurance premiums.

- Understanding the claims process involves prompt notification, documenting damage, and maintaining communication with insurers.

- Discounts for new homes, security systems, and policy bundling can lower insurance costs for Valley Stream residents.

- Regular policy reviews and home upgrades help balance affordability with comprehensive homeowners insurance coverage.

Policy Types

Homeowners insurance is available in several standardized forms, each defining covered perils and policy limitations. Selecting the correct form is a foundational step in risk management for your residence. The principal policy types are described below.

- HO-1 Basic Homeowner Policy: This policy offers limited coverage for specific perils, such as fire and theft, making it suitable for those on a tight budget.

- HO-2 Broad Homeowner Policy: This policy provides broader coverage than HO-1, including additional perils like falling objects and water damage from plumbing issues.

- HO-3 Special Homeowner Policy: The most popular type, HO-3 covers all perils except those specifically excluded, offering comprehensive protection for homeowners.

- HO-5 Comprehensive Homeowner Policy: This policy provides the highest level of coverage, protecting personal property against all perils unless explicitly excluded.

- HO-8 Modified Homeowner Policy: Designed for older homes, this policy covers the actual cash value of the home rather than the replacement cost.

Familiarity with these policy forms enables Valley Stream homeowners to align coverage structure with their risk profile and asset protection objectives.

Further research highlights specific considerations for HO-3 policies, particularly concerning flood hazard areas and liability exclusions.

HO-3 Homeowners Insurance & Flood Hazard Areas

Property owners in Special Flood Hazard Areas who purchase homeowners insurance should note that the HO-3 is the most common policy form; HO-3 policies, unlike HO-6 forms, may exclude certain liability coverages.

Insuring Justice, 2022

Coverage Options

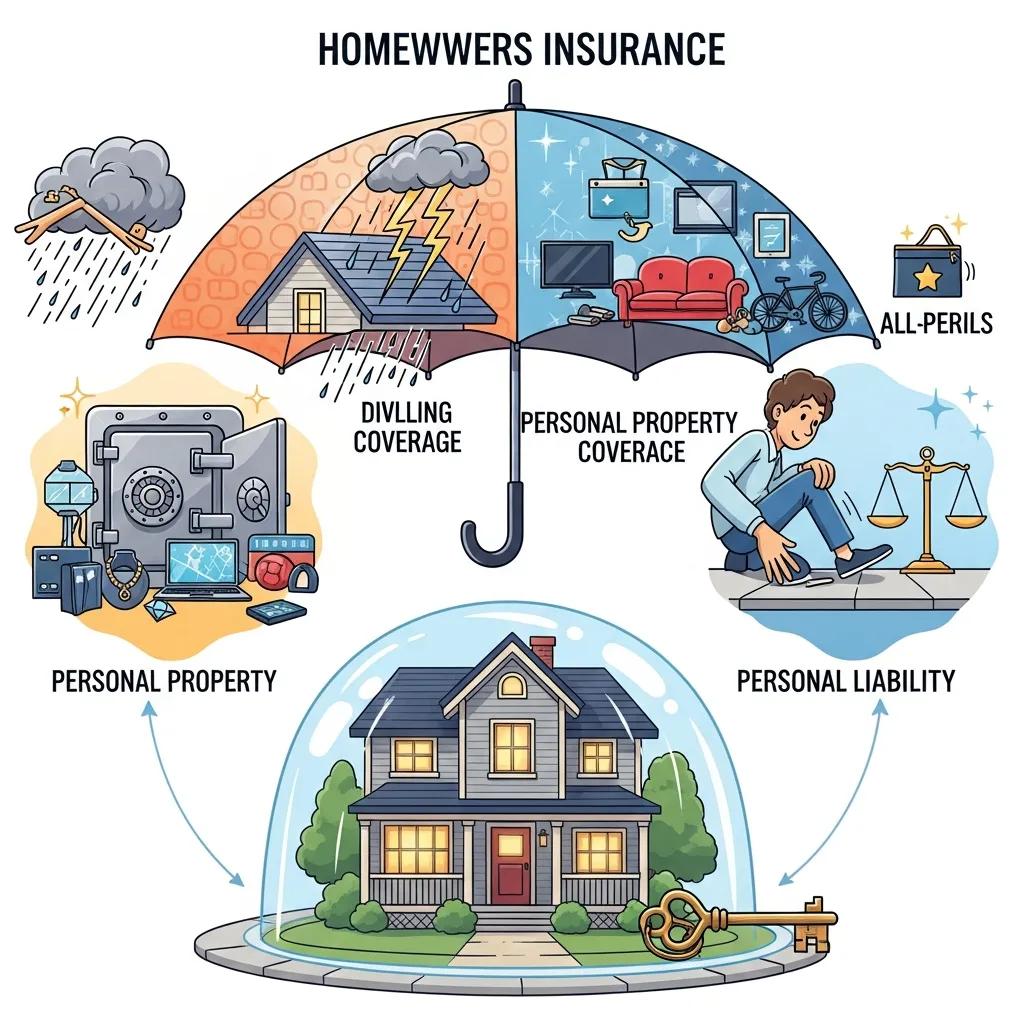

Coverage selection determines which losses are indemnified and the scope of insurer obligations. Key coverage components homeowners should evaluate include the structural, contents, and liability elements, as well as separate flood protection where required.

- Dwelling Coverage: This covers the structure of your home, including walls, roof, and built-in appliances, against damages from covered perils.

- Personal Property Coverage: This protects your personal belongings, such as furniture and electronics, from theft or damage.

- Liability Protection: This coverage protects you from legal claims if someone is injured on your property or if you cause damage to someone else’s property.

- Flood Insurance: Given Valley Stream’s location, flood insurance is crucial for homeowners, as standard policies typically do not cover flood damage.

Assess each coverage element against your exposure and asset value to customise limits and endorsements that address specific vulnerabilities.

Coverage Limits

Coverage limits define the insurer’s maximum payment for a covered loss and must reflect actual replacement and liability exposures. Selecting adequate limits prevents underinsurance and protects long-term financial security.

- Replacement Cost Coverage: This ensures that you can rebuild your home to its original condition without deducting for depreciation.

- Specialized Personal Property Coverage: High-value items, such as jewelry or art, may require additional coverage beyond standard limits.

- Liability Limits Customization: Homeowners should assess their risk exposure and consider increasing liability limits for added protection.

Set dwelling and contents limits based on replacement cost estimates and schedule high-value items to ensure claims reflect true market replacement costs.

Essential Considerations

Choosing an appropriate homeowners policy requires systematic evaluation of price, scope, and insurer capacity to respond to complex losses. Consider quotations, exclusions, and professional advice when structuring coverage.

- Requesting Multiple Quotes: It’s essential to compare quotes from different insurers to find the best coverage at the most competitive price.

- Understanding Exclusions: Be aware of what is not covered by your policy, such as certain natural disasters or specific types of damage.

- Consulting with Experts: Engaging with insurance professionals can provide valuable insights and help you navigate the complexities of homeowners insurance.

Applying these considerations helps Valley Stream homeowners secure policies that align with their asset protection objectives and risk tolerance.

What Are the Essential Homeowners Insurance Coverage Options in Valley Stream NY?

Coverage in Valley Stream should address coastal exposure, household contents, third‑party liability and, where applicable, separate flood protection. These coverages form the core of a comprehensive program.

- Dwelling Coverage: Protects the physical structure of your home from various perils.

- Personal Property Coverage: Safeguards your belongings against theft or damage.

- Liability Protection: Offers financial protection against legal claims resulting from injuries or damages on your property.

- Flood Insurance: Critical for homes in flood-prone areas, providing coverage for flood-related damages.

How Does Liability Coverage Protect Valley Stream Homeowners?

Liability coverage indemnifies homeowners for legal costs and awards arising from covered incidents. It protects personal assets and future earnings from claims tied to bodily injury or property damage for which the insured is legally responsible.

- Slip and Fall Accidents: If a visitor is injured while on your property, liability coverage can help cover medical expenses and legal fees.

- Dog Bites: If your pet injures someone, liability coverage can protect you from potential lawsuits.

- Property Damage: If you accidentally damage a neighbor’s property, liability coverage can help cover the costs.

Maintaining adequate liability limits and umbrella coverage where appropriate is essential to protect personal wealth from litigation risk.

What Flood Insurance Options Are Available for Coastal Properties?

Flood insurance is a distinct product from standard homeowners coverage. Homeowners should consider public and private options to secure financial protection against flood losses.

- National Flood Insurance Program (NFIP): This government-backed program offers flood insurance to homeowners in participating communities, providing coverage for flood-related damages.

- Private Flood Insurance: Some insurers offer private flood insurance policies that may provide additional coverage options or higher limits than NFIP policies.

- Eligibility Criteria: Homeowners must meet specific criteria to qualify for flood insurance, including the property’s flood zone designation.

Compare NFIP and private flood products for limits, waiting periods, and coverage features to determine the most suitable solution for coastal exposure.

Which Local Risk Factors Affect Homeowners Insurance in Valley Stream NY?

Local risk drivers in Valley Stream include coastal proximity, elevation relative to flood zones, and historical windstorm activity. These factors influence underwriting, premiums and required endorsements.

- Coastal Location: Homes near the coast are at higher risk for flooding and windstorm damage, which can affect insurance premiums.

- Flood Damage Exclusions: Many standard homeowners insurance policies exclude flood damage, making additional flood insurance necessary.

- Windstorm Coverage Considerations: Homeowners may need to purchase separate windstorm coverage to protect against hurricane-related damages.

Recognising these exposures allows homeowners to address coverage gaps and secure targeted protections where standard policies fall short.

This common exclusion of flood risk from standard policies represents a material coverage gap that must be addressed for coastal properties.

Homeowners Insurance Gaps: Flood Risk & HO-3 Policies

Homeowners insurance commonly excludes a range of risks; the flood exclusion is a primary example of such a coverage gap. The HO-3 Special Form provides standard coverage but does not remedy this particular exclusion.

Protection gaps in homeowners insurance, 2022

How Do Coastal Flooding and Windstorm Risks Impact Insurance Policies?

Coastal flooding and windstorm exposure affect policy design, endorsement needs and premium levels. Insurers assess these hazards when underwriting and may require specific wind or flood endorsements for adequate protection.

- Exclusion of Flood Damage: Most standard policies do not cover flood damage, necessitating separate flood insurance.

- Windstorm Damage Coverage: Homeowners may need to purchase additional coverage for windstorm-related damages, especially during hurricane season.

- Higher Premiums: Due to the increased risk, homeowners in coastal areas often face higher insurance premiums.

Accurately quantifying these risks and procuring appropriate endorsements or separate policies is necessary to maintain comprehensive protection.

What Mitigation Strategies Can Reduce Insurance Premiums?

Risk mitigation reduces loss frequency and severity and can translate to lower premiums. Insurers reward documented reductions in exposure with enhanced underwriting terms and discounts.

- Increasing Deductibles: Opting for a higher deductible can lower your premium, but be sure you can afford the out-of-pocket costs in the event of a claim.

- Installing Security Systems: Adding security features, such as alarms and surveillance cameras, can reduce the risk of theft and lower premiums.

- Participating in Community Flood Mitigation: Engaging in local flood mitigation efforts can demonstrate to insurers that you are taking steps to reduce risk, potentially leading to lower premiums.

Implementing structural and operational mitigation measures supports lower risk classifications and helps manage total insurance cost.

Beyond individual measures, coordinated strategies to mitigate coastal storm and hurricane risk are critical for sustained protection of vulnerable communities.

Coastal Storm & Hurricane Mitigation Strategies

Although significant obstacles impede effective hurricane and coastal storm mitigation, coordinated intergovernmental action has substantial potential to reduce exposure and improve community resilience.

Catastrophic coastal storms: Hazard mitigation and development management, DR Godschalk, 1989

What Are the Best Homeowners Insurance Providers and Programs for Valley Stream Residents?

Evaluate insurers on their ability to offer comprehensive coverages, specialist flood and windstorm options, and advisory service for complex loss scenarios. Coastal Insurance Solutions presents tailored programs for Valley Stream homeowners that address these requirements.

- Comprehensive Policies: Providing extensive coverage for various risks, including flood and windstorm protection.

- Personalized Service: Experts at Coastal Insurance Solutions can help homeowners navigate their options and find the best coverage for their needs.

- Competitive Rates: Coastal Insurance Solutions offers competitive pricing to ensure homeowners receive value for their insurance investment.

Selecting a provider with depth in coastal risk management and a track record of responsive claims handling materially improves coverage outcomes.

How Does the Homeowners Insurance Claims Process Work in Valley Stream NY?

Claims handling follows a defined process from notification to settlement. Prompt notification, thorough documentation and timely communication with your insurer are essential to an effective recovery.

- Notify Your Agent: As soon as damage occurs, contact your insurance agent to report the claim.

- Document the Damage: Take photos and gather evidence of the damage to support your claim.

- Follow Up on the Claim: Stay in contact with your insurer to ensure your claim is processed efficiently.

Familiarity with insurer requirements and documented proof of loss expedites assessment and settlement.

What Are the Step-by-Step Procedures for Filing a Claim?

Filing a claim requires a structured approach: notify the insurer, compile supporting documentation, and facilitate the adjuster’s inspection. Each step supports an accurate loss valuation.

- Notify Your Agent Promptly: Contact your insurance agent as soon as possible to report the incident.

- Gather Required Documentation: Collect necessary documents, including photos of the damage and any relevant receipts.

- Schedule an Adjuster’s Visit: Your insurer may send an adjuster to assess the damage and determine the claim amount.

Adhering to the insurer’s documentation checklist and cooperating with the adjuster improves the likelihood of a timely and fair settlement.

How Can Homeowners Ensure Efficient and Successful Claim Resolution?

Proactive mitigation, detailed records and consistent communication materially improve claim outcomes. Preserve evidence and promptly address secondary risks to limit further loss.

- Prevent Further Damage: Take immediate action to mitigate additional damage, such as covering broken windows or shutting off water sources.

- Document Everything: Keep detailed records of all communications with your insurer and any expenses incurred due to the damage.

- Stay in Contact with Your Insurer: Regularly follow up with your insurance company to check on the status of your claim.

Organized documentation and clear communication reduce disputes and accelerate claim resolution.

What Discounts and Cost-Saving Strategies Are Available for Valley Stream Homeowners Insurance?

Insurers provide a range of discounts tied to construction standards, safety systems and policy consolidation. Identify applicable credits to lower premiums without sacrificing material protections.

- New Home Discounts: Many insurers offer discounts for newly built homes, as they often have modern safety features.

- Security System Discounts: Installing security systems can lead to significant savings on premiums.

- Bundling Policies for Savings: Combining homeowners insurance with other policies, such as auto insurance, can result in additional discounts.

Quantify available discounts and apply those savings to improve coverage quality or reduce out-of-pocket exposure.

Which Discounts Can Lower Premiums for Coastal Property Insurance?

Coastal risks increase premiums, but targeted discounts—such as for modern construction, long-term customer tenure and reduced internal hazards—can offset costs. Assess eligibility with your insurer.

- Discounts for New Homes: Newly constructed homes often qualify for lower rates due to their updated safety features.

- Carrier Longevity Discounts: Long-term customers may receive loyalty discounts for staying with the same insurer.

- Non-Smoker Discounts: Homeowners who do not smoke may qualify for additional discounts, as non-smoking homes are generally considered lower risk.

Applying available discounts strategically enables homeowners to manage premiums while retaining comprehensive coverages.

How Can Homeowners Balance Affordability with Comprehensive Coverage?

Balancing cost and protection requires analysis of deductible strategy, periodic policy reviews and targeted home improvements that reduce risk. Decisions should reflect both budgetary constraints and asset protection priorities.

- Choosing Higher Deductibles: Opting for a higher deductible can lower monthly premiums, but ensure you can afford the out-of-pocket costs in case of a claim.

- Regularly Reviewing Policies: Periodically reassessing your coverage needs can help identify areas where you can save money without sacrificing essential protection.

- Upgrading Home Features: Investing in home improvements, such as storm-resistant windows, can reduce risk and potentially lower insurance premiums.

Regularly review coverage, apply eligible discounts and invest in mitigation to sustain both affordability and robust protection.

For those with significant assets, high value home insurance delivers enhanced limits and bespoke policy features designed for elevated exposures.

Additionally, high net worth insurance provides comprehensive programs that address the complex needs of affluent individuals.

Furthermore, insurance for high net worth individuals is structured to protect valuable assets and preserve financial security against large or complex losses.

Frequently Asked Questions

What factors should I consider when choosing homeowners insurance in Valley Stream?

Consider local hazard exposure, applicable policy forms, coverage limits, and exclusions. Evaluate replacement cost estimates for the dwelling, contents limits, liability capacity and the need for separate flood or windstorm coverage. Obtain competing quotations and review insurer solvency and claims performance.

How can I determine the right coverage limits for my homeowners insurance?

Estimate the replacement cost of the dwelling using professional appraisals or contractor estimates. Inventory personal property and identify high‑value items for scheduled coverage. Assess liability exposure relative to net worth and potential litigation risk, and adjust limits or add an umbrella policy accordingly.

What should I do if my homeowners insurance claim is denied?

Review the denial notice and policy language to identify the basis for denial. Submit additional documentation where applicable and request a detailed explanation from your agent or claims representative. If resolution is not achieved, consider consultation with a public adjuster or legal counsel to pursue an appeal.

Are there specific insurance requirements for rental properties in Valley Stream?

Yes. Landlords typically require landlord insurance that covers the building, liability and rental income loss. Tenants should carry renters insurance for personal property and liability. Confirm any municipal or mortgage lender requirements and consult an insurance professional to ensure compliance.

How often should I review my homeowners insurance policy?

Review your policy annually and after material changes such as renovations, major purchases or changes in occupancy. Annual reviews ensure limits reflect current replacement costs and that endorsements or new products address evolving exposures.

What are the benefits of bundling homeowners insurance with other policies?

Bundling can produce premium discounts, simplify policy administration and improve coordination of coverages across multiple lines. Insurers may offer broader terms or enhanced service to customers who consolidate policies with the same carrier.

What steps can I take to prepare for a potential insurance claim?

Create a detailed home inventory with photos and receipts, store records securely offsite or in the cloud, and familiarise yourself with policy coverages and claim procedures. Keep your agent’s contact information readily available and document any damage promptly to support a claim.

Conclusion

Understanding homeowners insurance in Valley Stream is essential to protect property and financial assets from local hazards such as flooding and windstorms. Select appropriate policy forms, set limits to reflect replacement cost and liability exposure, and address coverage gaps with separate flood or windstorm products as required. Compare quotes and consult a trusted insurance professional to secure a program tailored to your needs.